Student Cases

Quant

Quant

Can You Break Into Citadel Securities Quant Trading Without a Math Olympiad

I came into quant recruiting without a single Olympiad medal on my resume. For months, I thought that meant I'd already lost. What I didn't realize was that market makers care less about the medals than about how you think when you don't know the answer.

Published on

May 27, 2026

6

min read

I grew up in a quieter coastal town where nobody around me was prepping for math competitions in elementary school. When I transferred to a competitive high school at fourteen, I realized most of my new classmates had been training for Olympiads since they were nine.

I never caught up on that front. I spent a semester abroad in Eastern Germany during a stretch of the pandemic, which was the first long block of solitude I'd ever had. I read biographies of Jobs, Musk, Dalio, and Feynman, and started teaching myself college physics from PDFs I found online. That habit followed me to UCLA, where I declared applied math, then to Columbia, where I transferred for my sophomore year.

This case study walks through how I got from there to a 2026 summer offer from Citadel Securities for Quant Trading in New York.

1. From Applied Math at UCLA to Columbia: Why I Transferred

1.1 Why UCLA Wasn't the Right Launchpad for Quant

UCLA's intro physics and CS classes were genuinely good. The problem wasn't the teaching. The problem was scale. Required courses filled up in minutes. Office hours were standing room only. Research positions in the math department were rationed across hundreds of applicants. I could see myself spending two more years fighting for resources that East Coast students at smaller schools were getting handed to them.

There's also a geographic reality nobody told me until I was already in California. The recruiting cadence for quant trading runs through New York. Info sessions, coffee chats, on-campus events at Citadel Securities, Jane Street, Hudson River Trading, Optiver, and SIG happen there. Flying in for a single networking event is doable. Building real relationships from 3,000 miles away is not.

By the end of my freshman year I'd made up my mind. I rewrote my essays over winter break and applied to several East Coast schools.

1.2 What Columbia Opened Up

Columbia gave me three things UCLA couldn't. Proximity to recruiters. A smaller applied math cohort where TAs actually knew my name. And a peer group already deep into quant prep. By my second week on campus, I'd been pulled into a study group running through Frederick Mosteller's Fifty Challenging Problems in Probability.

That single shift in environment moved my preparation timeline forward by about a year.

2. The Quant Trading Path Most Students Misunderstand

2.1 Why Wall Street Is Hiring More Mathematicians Than Finance Majors

The first time I read a profile of how Citadel Securities recruits, I had to recheck the source. According to a 2023 Fortune profile of the firm's internship program, Citadel and Citadel Securities received roughly 69,000 internship applications that year, and the interns selected came almost exclusively from math, physics, and CS backgrounds. MBAs, the article noted, rarely made the cut.

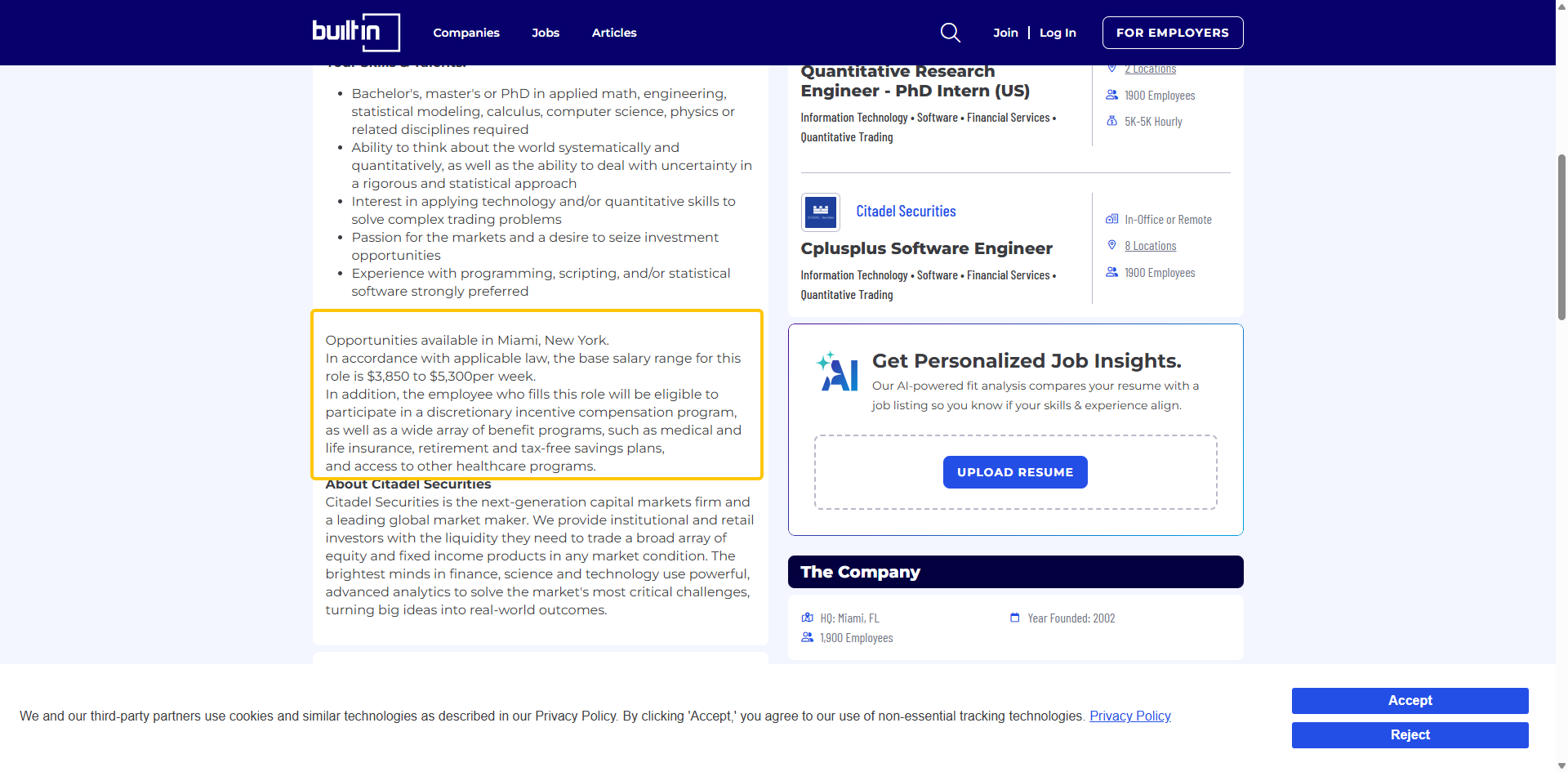

Compensation reflects the same pattern. According to a Citadel Securities 2025 official job posting, the base salary range for Quantitative Trading interns runs from $3,850 to $5,300 per week. That's posted directly by the firm, not estimated by an aggregator.

What I took from this wasn't "go become a mathematician." It was simpler. The bar for market making roles is technical, but the technical bar is one you can train for outside of competition pipelines if you start early enough and work in the right direction. This sits inside broader shifts in finance careers that have been quietly redrawing the map of who Wall Street hires.

2.2 What Market Makers Actually Look For

Market makers post bid and ask prices on financial instruments and earn the spread, while managing the inventory risk they take on. The skill set that maps to this work isn't memorized derivatives theory. It's three things layered on top of each other.

The first is fast, accurate mental arithmetic under social pressure. The second is calibrated probabilistic reasoning, meaning you can estimate quantities you don't know and update your estimates cleanly as new information arrives. The third is decision-making under incomplete information, the actual core of market making.

Olympiad winners often have the first two. They don't necessarily have the third, and the third is what gets tested hardest in a Citadel Securities interview. These map closely to the most in-demand technical skills showing up across high-paying roles right now.

3. The Self-Doubt of Competing Against Olympiad Winners

3.1 Reading Resumes That Made Me Question My Start

Halfway through sophomore year, I started reading LinkedIn profiles of people who'd landed offers at the firms I was targeting. The pattern was consistent and discouraging. The same Fortune profile I'd read for inspiration also reported that successful interns at Citadel come "almost without exception" from the most prestigious universities in their regions, with some holding math Olympiad gold prizes or math doctorates from Stanford.

I was a transfer student with an applied math major, two unremarkable internships, and zero competition medals. Kristina Martinez, Citadel's managing director for human resources in Asia-Pacific, was quoted in the same article describing the candidate pool as "a finite pool of truly exceptional students." I was not in that pool, or at least I couldn't prove I was.

The dominant feeling that semester was that the gap had been set years before I knew the game existed.

3.2 When DIY Recruiting Stopped Working

I'd been recruiting on my own for about a year. My resume had two internships, a TA position, and a couple of research projects. I'd been applying to OAs and getting auto-rejected. I'd been emailing alumni and getting polite no-replies.

A close friend of mine had taken a different path. He'd worked with One Strategy Group through his sophomore recruiting cycle and landed an investment banking offer at a target firm. He'd been pointing me toward structured recruiting support for months. I'd been resistant to the idea of mentorship for over a year, partly out of pride and partly because I wanted to prove I could do this alone. By February of sophomore year, with one quant cycle effectively burned, I let the pride go.

4. Working with One Strategy Group: Two Tracks, One Focus

4.1 A Backup S&T Offer Bought Me Time to Bet on Quant

When I joined One Strategy Group, I was assigned two mentors. Steven covered Sales & Trading, and Victor covered Quant Trading. The S&T timeline runs earlier than quant, so we worked on that track first. Within a few months, Steven helped me land an S&T summer offer at a bulge bracket bank.

That offer changed everything about how I approached the quant cycle. It wasn't because S&T was my goal. It was because the offer removed the financial and emotional pressure to "win" the quant cycle on the first try. I could afford to bet hard on a low-probability outcome, which is what landing a quant trading offer without a competition background was.

This is the part of One Strategy Group mentorship that I hadn't expected. The first measurable result wasn't the dream offer. It was the safety net that let me chase the dream offer.

4.2 How Victor's Mock Interviews Reframed My "Weakness"

Victor came from a math competition background and currently traded at a top market maker. Our first mock was forty-five minutes of probability puzzles, mental math drills, and one trading game. I expected him to confirm what I'd already concluded about myself.

He didn't. His feedback after the mock was that my structured problem-solving was strong, my mental arithmetic was average and trainable, and my biggest weakness was that I apologized for not knowing things instead of estimating and committing. He told me competition kids have a specific advantage in raw speed, but they also have specific weaknesses, and the weaknesses are visible to good interviewers.

That single mock reframed the next six months of my preparation. I wasn't trying to become an Olympiad winner. I was trying to become a market maker, which is a different job.

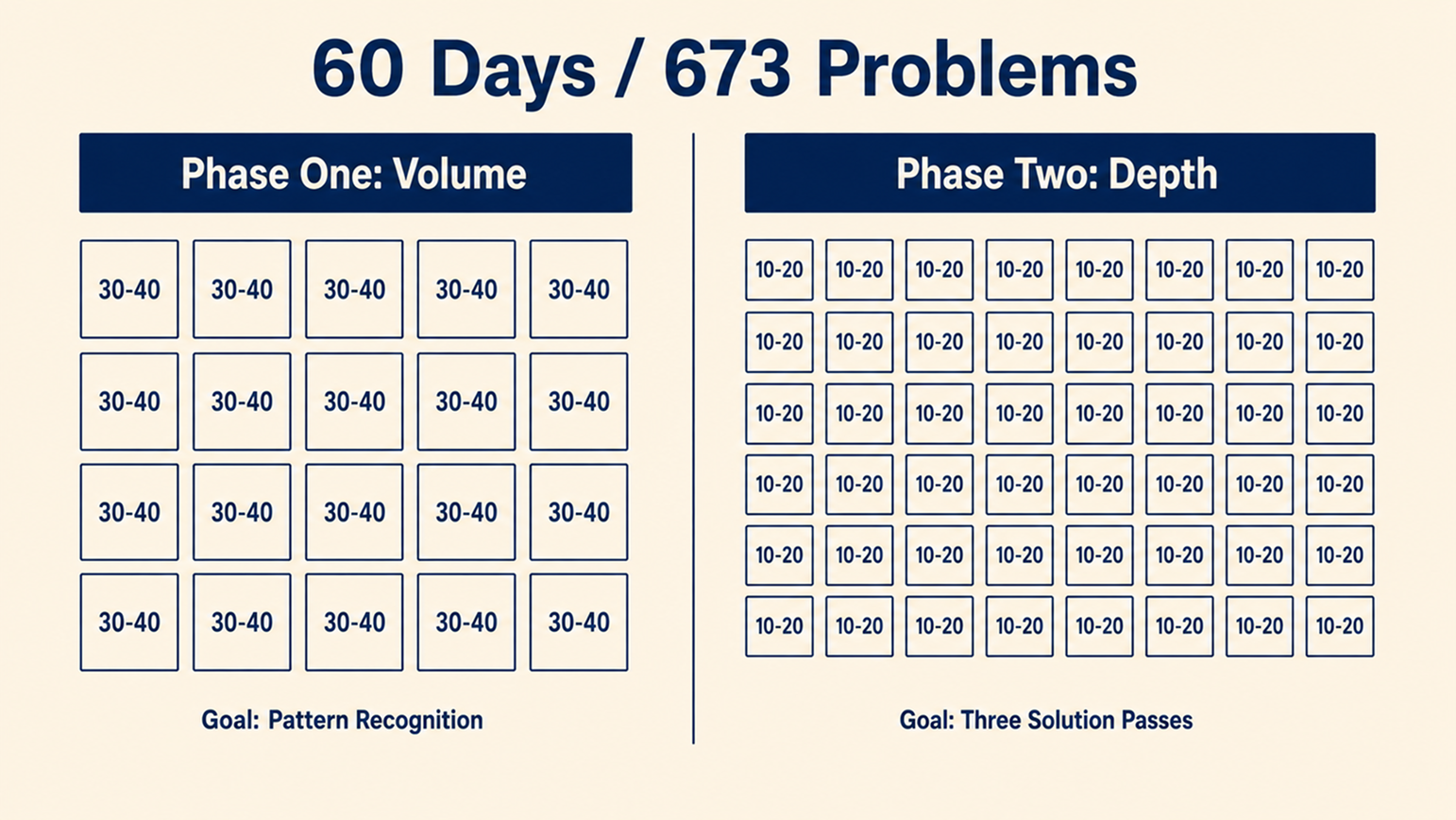

5. The Summer of 673 Problems

"Five notebooks. 673 problems. One summer in New York while most of my friends went home. I wasn't drilling for the sake of drilling. I was learning to recognize the shape of a problem before I'd finished reading it."

Victor and I built a study plan in late May. I was TAing a graduate summer course at Columbia three afternoons a week, so the plan had to fit around that. The structure he proposed for One Strategy Group career coaching followed three phases.

5.1 Phase One: Volume Over Polish

The first twenty days were pure volume. Thirty to forty problems a day, drawn from a rotating set of probability puzzle banks, brainteaser archives, and old interview question collections. The point wasn't to solve every problem. It was to see enough problems that I started recognizing categories. Two coins versus three coins. Conditional probability with asymmetric information. Expected value with stopping rules.

By day twenty I could read a problem and place it into a family within about ten seconds. That recognition speed turned out to matter more than any individual solution.

5.2 Phase Two: Deep Pattern Recognition

The next forty days shifted from volume to depth. Ten to twenty problems a day, each one solved three ways. First my own solution. Then the canonical solution. Then a third pass where I tried to generalize, asking what assumption I could change to make the problem harder, and whether the technique transferred to a different family.

This is where the notebooks filled up. Five composition books by the end of August, 673 problems total. The number isn't impressive on its own. What mattered was that by the end I was reading new problems with a different brain.

5.3 Beyond Drilling: Market Making Theory

Pure puzzle drilling has a ceiling. Around mid-July, Victor and two other quant mentors at One Strategy Group started layering in market making theory. Bid-ask spread mechanics. Inventory risk and skewing quotes. The Kelly criterion and its limits. Adverse selection in a fragmented market.

This was the connective tissue. The puzzles had been teaching me to compute probabilities. The theory taught me what to do with those probabilities when there's money at stake and someone on the other side knows something you don't.

6. Inside the Citadel Securities Interview Process

6.1 The Online Assessment

The OA came in late July. Fifteen questions in thirty minutes, heavy on probability and quick mental math. I'd done enough timed drills by then that the format itself wasn't the obstacle. The obstacle was choosing which two or three questions to skip cleanly to protect time on the rest.

Then I waited a month. The hardest stretch of the entire process was the silence between submission and the first-round invite on August 29th.

6.2 Trading Games and Group Rounds

The first technical round was a ninety-minute group interview with four other candidates and two interviewers. The structure was a multi-round trading game with a deck of cards standing in for a market, partial information distributed across the group, and live price updates.

This is where Victor's training paid off in the most concrete way. He'd run me through a simplified version of this exact game format four times in the preceding weeks. The first time I'd lost money in every round. By the fourth I was breaking even and starting to read the other players. In the actual interview, I wasn't trying to win every round. I was trying to demonstrate that I could update my pricing as new information came in and explain my reasoning out loud while I did it. A lot of what I leaned on came from preparing for the four essential parts of any interview and treating each round as a separate performance.

The two follow-up rounds were forty-five minutes each, technical and behavioral mixed. Probability questions, a brainteaser, a discussion of one project from my resume, and a deliberately open question about a market I'd been watching.

6.3 The Superday and the Steakhouse Dinner

The Superday in early October was three technical rounds back to back, then a group dinner at a steakhouse near the office. My brain was fully cooked by the time we sat down. I'd assumed dinner was another evaluation stage.

It mostly wasn't. The interviewers stopped asking technical questions and started talking about apartments, neighborhoods, and where to eat in the city. One of them asked about my football background and mentioned that a senior trader on the desk had played college ball. He offered to set up a Giants game when I started. That was when I understood that the technical bar was a filter, and what they were trying to assess at dinner was whether I was someone the desk would want to sit next to for ten hours a day.

The call came the following Monday afternoon. Quant Trading, summer 2026, New York.

7. What I'd Tell Anyone Starting From Zero

The most useful question Citadel asked me wasn't a brainteaser. It was a behavioral one at the Superday: tell me about your five greatest achievements.

I'd expected to list technical wins. What I actually talked about was earning the trust of teammates on a sports team where I started as the worst player, teaching graduate students as a sophomore TA, and learning to contribute production code on a project where I started the week not knowing the language. None of those things would show up on a competition resume. All of them were closer to the actual job than any single probability puzzle I'd solved.

If you're a year or two out from quant recruiting and you don't have a competition background, here's the version I wish I'd heard at the start. The medals matter less than the recruiters' websites suggest. The work, the volume of focused practice, and the willingness to be coached matter more. The same patterns show up across other student case studies on this site. And the highest-leverage decision I made in the entire two years wasn't transferring schools or picking a major. It was letting someone with a clear view of the process help me build a plan and hold me to it. That's what One Strategy Group did, and it's the part I'd repeat without hesitation.

Disclaimer: One Strategy Group has no partnership or affiliation with Citadel Securities or any other firm mentioned in this case study. All OSG students secure offers through standard campus or industry recruiting channels after working with OSG to develop their skills and preparation.

Free Career Planning Session

Book a free 1-on-1 session with an OSG mentor and map out your path to top firms!

Book Your Free Session →Ready to Write Your Own Success Story?

Book a free 1-on-1 session with an OSG mentor and map out your path to top firms!

Book Your Free Session →Explore More Resources

Frequently Asked Questions

Yes. While many quant traders have Olympiad or PhD backgrounds, market makers like Citadel Securities also hire candidates who demonstrate strong probabilistic reasoning, mental math, and decision-making under uncertainty. Structured drilling, market making theory, and trading game practice can substitute for competition experience over a focused 6-month preparation window.

There is no fixed number, but a focused preparation cycle often involves several hundred problems across probability puzzles, brainteasers, and mental math drills. The featured case study reached 673 problems over one summer, split between a high-volume recognition phase and a deeper pattern-analysis phase that included three solution passes per problem.

One Strategy Group pairs students with mentors who currently work in target industries such as quant trading, sales and trading, investment banking, and consulting. Its coaching covers resume positioning, technical preparation, mock interviews, and offer-stage strategy. It is most useful for students recruiting for highly selective programs without strong internal referrals or established alumni networks.

.jpg)