Student Cases

Quant

Quant

Rebuilding Resume and Recruiting Strategy Mid-Cycle to Land D.E. Shaw

Recruiting felt like the kind of game where you don't win by being the strongest at the start. You win by staying in long enough to figure out what the game is actually asking of you. Most people quit before that part.

Published on

May 25, 2026

6

min read

Most recruiting advice for quant hedge funds tells you to grind technicals and memorize answers. That worked for me until my first mock interview, when an interviewer cut me off mid-sentence and asked me to reframe my entire thesis. I had three minutes to figure out that the prep I'd been doing was the wrong prep.

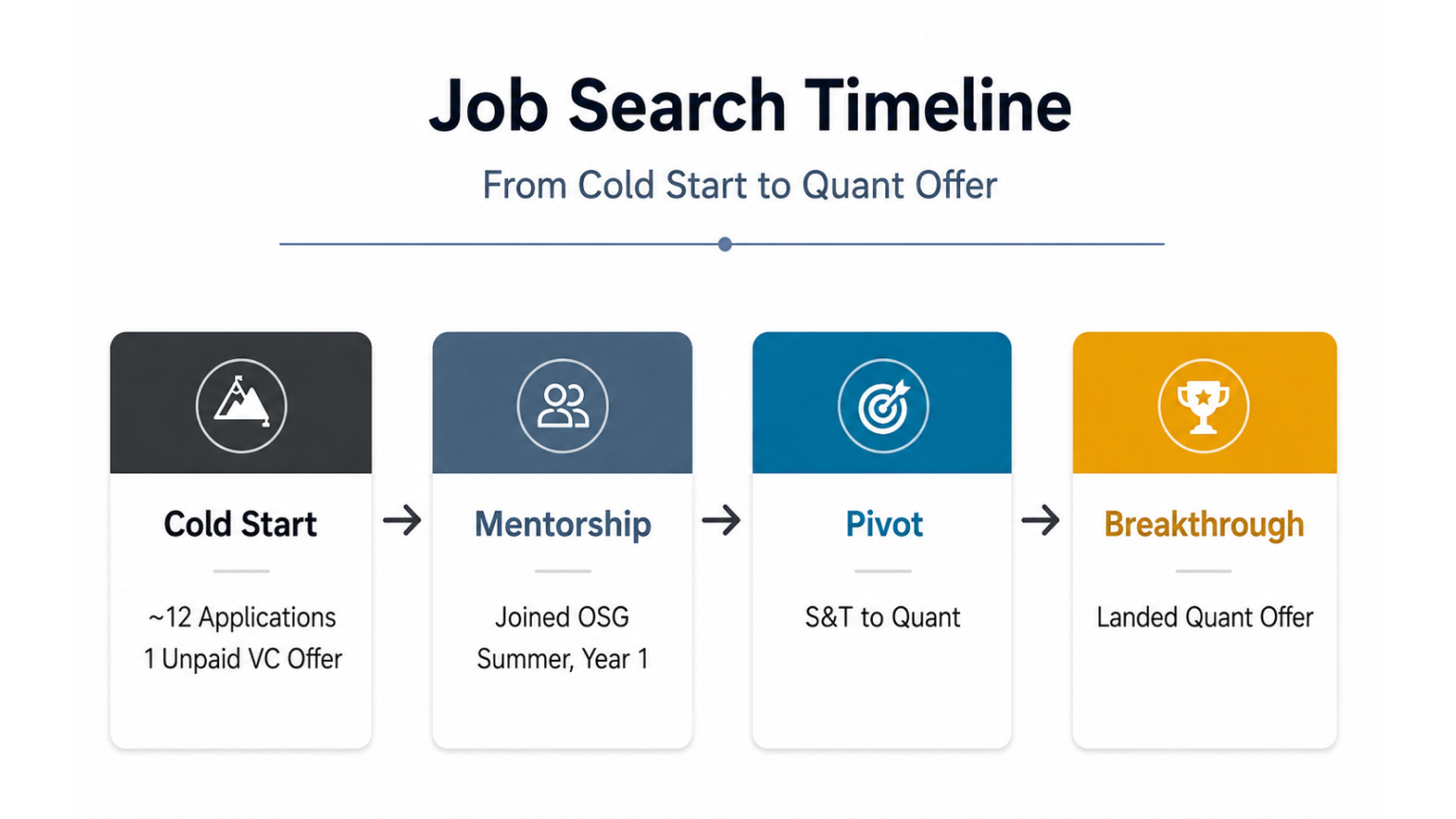

This is the story of how I went from sending applications into the void and getting one unpaid VC offer back, to closing three offers in a single recruiting cycle — including D.E. Shaw. I switched target roles mid-prep, rebuilt my resume twice, and learned that D.E. Shaw recruiting rewards people who can think out loud under pressure, not people with the cleanest scripts.

From Math Competitions to Hedge Fund Curiosity

I came to finance late. Through most of high school, my real obsession was math competitions and the kind of fast-reaction games where reps matter more than talent. I logged something close to 10,000 hours on those games. At some point the technical ceiling stopped moving, and what separated wins from losses was reading the situation faster than the other person. That lesson stuck with me longer than the games did.

Why Math Stopped Feeling Like the Whole Answer

Math was the academic version of the same thing. I liked breaking a problem into pieces and pushing toward the layer underneath. I thought research would be the natural endpoint. The problem was that research moves slowly, and I wanted to work on something where the feedback loop was faster and the variables kept changing.

The High School Investment Club That Changed Everything

The investment club at my high school was the first place I saw the same decomposition instinct applied to markets. People assume markets are random until they sit down and try to model one. They aren't. The pricing logic is messier than a math problem, but the structure is recognizable once you start pulling on it. That was the moment I stopped thinking of finance as a backup plan and started thinking of it as the actual fit.

The Cold Start: Sending Applications Into the Void

The decision was easy. The execution wasn't.

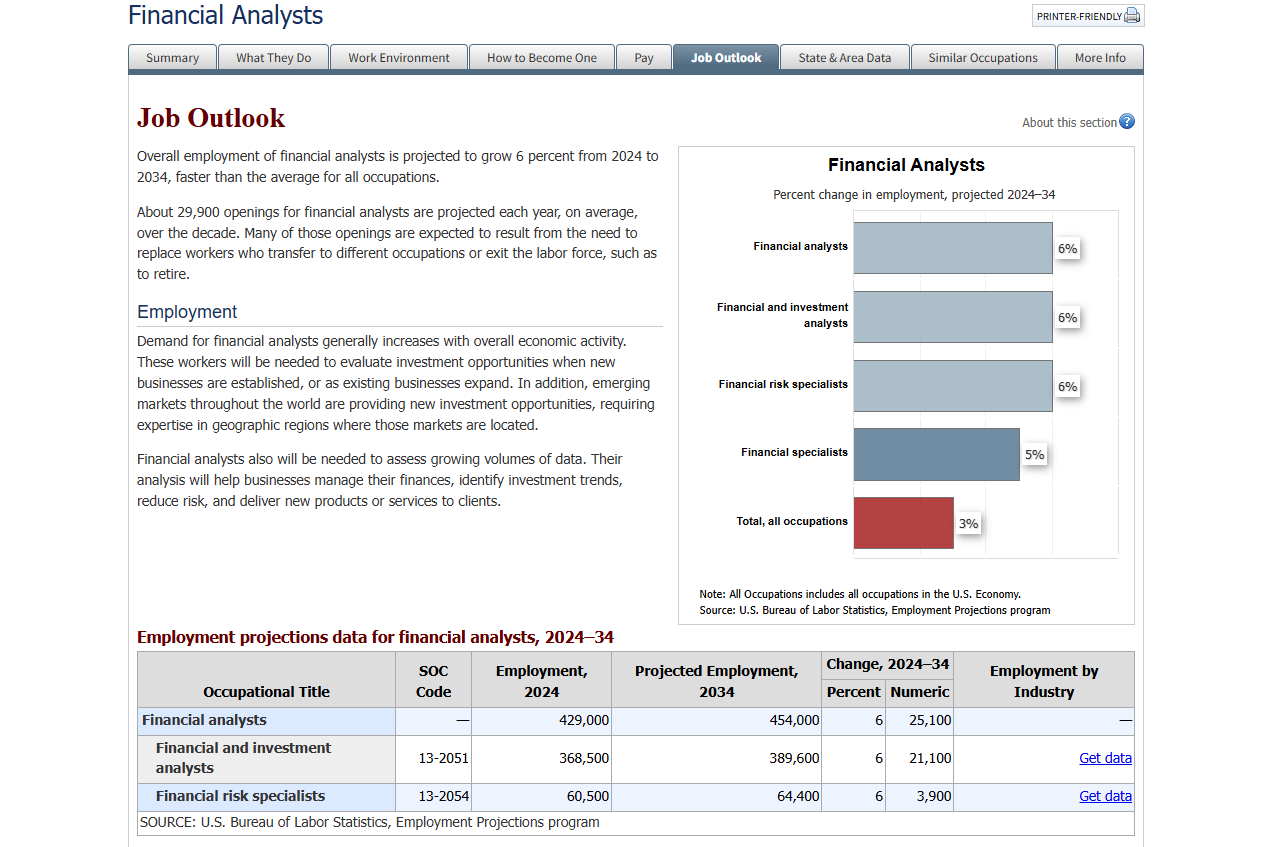

I sent applications to somewhere around a dozen firms during my freshman year. Most days I'd refresh my inbox and find a marketing email or an automated rejection. The one offer I landed was a remote, unpaid VC internship. The broader market for careers in finance is competitive even in good years. According to the U.S. Bureau of Labor Statistics, financial analyst employment is projected to grow 6 percent from 2024 to 2034, nearly double the 3.1 percent projected growth rate for the overall U.S. workforce over the same period. But those openings sit across the whole industry — not concentrated at the buy-side seats most students actually want.

What Networking Looked Like When I Had No Idea What I Was Doing

I was trying to prepare for interviews I wasn't getting. I didn't know how to ask for a coffee chat without sounding like a script. When someone actually replied, I didn't know what to ask them. The mechanics of building a relationship with a working professional — what to send, when to follow up, what to say in a thirty-minute call — none of that was obvious from the outside. I was treating networking like a transaction when it's closer to apprenticeship.

Finding a Framework Through One Strategy Group Mentorship

I first heard about One Strategy Group at a campus event where CMU students talked through their actual recruiting timelines. What got my attention wasn't the offer list. It was that the people on the panel had thought carefully about why certain prep moves had worked and others hadn't. A few friends pushed me to look more seriously, and when I looked through past One Strategy Group mentorship outcomes, I noticed something that mattered to me: a lot of students placing well didn't come from the obvious target schools. I signed up the summer after freshman year.

My first mentor, Anthony, started me on sales and trading (S&T), the desk-based role where banks buy and sell securities for clients, because that's where I told him I was leaning. He came from a hedge fund background, and the more we talked through how different desks operated, the more I realized S&T wasn't actually what I wanted. The roles that fit me — the ones that rewarded curiosity, mathematical judgment, and pattern recognition under uncertainty — were at firms like Citadel and D.E. Shaw, where computational finance and quantitative methods drive the investment process.

Why I Pivoted From Sales & Trading to Quant Hedge Funds

The pivot felt obvious in retrospect. S&T had been a placeholder for "I want to be close to markets." Quant hedge funds were closer to what I actually wanted to do, which was use math to find edges that other people hadn't priced in yet. The hard part wasn't the realization. It was rebuilding my prep from scratch six months in.

What Tier 1 Hedge Fund Interviews Actually Test

Once the target changed, I had to figure out what quant hedge fund recruiting actually looked like. There wasn't a clean playbook for it. Top quant hedge funds are widely understood to be among the most selective seats in finance, and what I saw in practice matched that reputation.

My One Strategy Group career coaching mentor helped me build the map: which research blogs to follow, which authors were worth tracking long-term, how different fund types actually made money. The three main ones worth knowing: multi-strat funds run multiple investment strategies under one roof to diversify risk, systematic funds let algorithms and models make the trading decisions, and discretionary macro funds rely on human judgment about big-picture economic shifts. Scattered information turned into something usable.

The Mock Interview That Humbled Me

I walked into my first mock thinking technical prep and clean answers would carry me. Within ten minutes I understood why that wasn't enough. The interviewer didn't follow my structure. He followed my answers. Every time I finished a point, the next question pulled at the weakest part of what I'd just said. "What if the conditions changed?" "What's the assumption you're building on?" My rhythm broke. I got stuck.

That's when I understood what these interviews actually test. It isn't a perfect answer. It's whether you can hold a thread of reasoning while someone is actively pulling on it, and whether you stay clear under pressure. The same logic applies to the superday, the final round at most banks and funds where candidates run through back-to-back interviews with senior staff in a single day.

Rebuilding My Resume Around Real Evidence

The resume rebuild was the other unlock. My mentors didn't let me fill it with jargon. We went line by line and asked what I had actually done and what I could prove. The behavioral prep ran on the same logic — instead of memorizing answers, we mapped my real experiences into eight or nine stories that could flex to fit most questions. My self-introduction stopped sounding like a template and started sounding like a person whose math and finance backgrounds actually connected.

By the time real interviews started, I was less nervous than during the mocks. The format I had been afraid of — interviewers jumping topics, interrupting, stacking follow-ups — was what I had spent months preparing for.

Three Offers Later: What I'd Tell Someone Starting Out

I closed three offers that cycle. The D.E. Shaw seat was the one I wanted. The bulge bracket offers — meaning offers from the largest global investment banks like Goldman Sachs, Morgan Stanley, and JPMorgan — were validation that the rebuild had worked across the board.

Three things I'd tell someone earlier in the process:

1. Find the role that actually fits your skill stack. Not the role with the highest prestige score in your friend group. The cost of being in the wrong seat compounds.

2. When you're in the room, bring some warmth. Interviewers at this level talk to a lot of technically competent people. The ones who get remembered are the ones who think well and are easy to talk to.

3. Treat recruiting like a long game. Most people who don't make it didn't run out of ability. They ran out of patience and quit the round before the one that would have worked.

The Long Game: Running, Gaming, and Recruiting

In middle school, I was one of the faster runners in my school. Then the pandemic happened, training stopped, and when I came back to the track I'd lost it. I almost didn't make the team.

I trained back into it. Slowly at first, then to where I'd been before. That's the pattern for me. Once I've decided what I'm going for, I don't quit the race.

If life is a game, I'm the player who doesn't start at the top of the leaderboard. I'm the one who keeps showing up to grind levels until the rankings catch up.

This round, I wanted first place.

Note: One Strategy Group is not affiliated with any of the firms named in this article. Students featured in One Strategy Group case studies receive coaching and preparation support, and pursue offers through standard recruiting channels on their own merit.

Free Career Planning Session

Book a free 1-on-1 session with an OSG mentor and map out your path to top firms!

Book Your Free Session →Ready to Write Your Own Success Story?

Book a free 1-on-1 session with an OSG mentor and map out your path to top firms!

Book Your Free Session →

Frequently Asked Questions

D.E. Shaw ranks among the most selective seats in quantitative finance. Successful candidates typically combine strong math backgrounds with the ability to reason clearly under interview pressure.

Probability, statistics, linear algebra, and calculus are standard expectations. Competition experience helps but isn't required — what matters more is the ability to explain your reasoning out loud.

Most candidates begin serious networking and skill-building the summer after freshman year. The case study above reflects that timeline, with offers closing during the junior recruiting cycle.

.jpg)